Toggle navigation

About Me

Scholarship

Teaching

Service

Blog

Contact Me

By using our site you agree to our use of cookies to deliver a better site experience. Find out more

here

.

Reject

Accept

All Posts With Tag NFIP

2018

Wednesday July 11, 2018

Flood Insurance Reauthorization

•

environmental policy

•

flood insurance

•

NFIP

•

political process

•

Monday July 09, 2018

Interview in the Extra Mile

•

environmental studies

•

flood insurance

•

NFIP

•

press clippings

•

Tuesday February 13, 2018

Flood Insurance Renewed...Again

•

budget

•

environmental studies

•

flood insurance

•

NFIP

•

2017

Monday September 04, 2017

Editorial on Texas Flooding in the News and Record

•

environmental studies

•

flood insurance

•

Hurricane Harvey

•

NFIP

•

Thursday August 31, 2017

Audio from The Attitude Interview

•

environmental justice

•

environmental policy

•

environmental studies

•

flooding

•

Houston

•

NFIP

•

Tuesday August 29, 2017

Listen Live on Thursday, 8/31

•

environmental justice

•

environmental studies

•

flood insurance

•

Hurricane Harvey

•

interviews

•

NFIP

•

press

•

radio

•

Friday May 05, 2017

New Court Decision on Flood Insurance

•

environmental policy

•

environmental studies

•

Fourth Circuit

•

insurance

•

legal decisions

•

NFIP

•

Tuesday April 25, 2017

Implications of Coarse Data Allocation Methods for Flood Mitigation Analysis

•

data science

•

demography

•

environmental policy

•

environmental studies

•

flood insurance

•

mathematics

•

NFIP

•

working papers

•

Friday April 14, 2017

California Flood Insurance Hurts Everyone

•

California

•

environmental economics

•

flood insurance

•

insurance

•

NFIP

•

2016

Friday June 03, 2016

FEMA's Flood Maps Are Not a Scam

•

environmental justice

•

environmental policy

•

environmental science

•

environmental studies

•

FEMA

•

flood insurance

•

flood studies

•

NFIP

•

Sunday May 29, 2016

Flood Insurance Profits? Maybe Not

•

environmental policy

•

environmental studies

•

finance

•

flood insurance

•

flood studies

•

insurance

•

news

•

NFIP

•

Wednesday May 11, 2016

The Private Flood Insurance Bill

•

environmental policy

•

environmental studies

•

flood studies

•

insurance

•

NFIP

•

risk management

•

Friday May 06, 2016

My Dissertation

•

environmental policy

•

environmental studies

•

flood studies

•

NFIP

•

UMBC

•

Tuesday May 03, 2016

Socioeconomic Effects of the National Flood Insurance Program is now available

•

books

•

environmental policy

•

environmental studies

•

flood insurance

•

flood mitigation

•

NFIP

•

research

•

UMBC

•

Tuesday March 29, 2016

Learn About Flood Insurance When Renting

•

environmental policy

•

environmental studies

•

flood studies

•

insurance

•

interviews

•

NFIP

•

press

•

risk management

•

Thursday February 11, 2016

Pennsylvania's Flood Insurance Exchange

•

environmental policy

•

environmental studies

•

flood insurance

•

NFIP

•

Friday January 29, 2016

RFFs Parametric Flood Insurance Proposal

•

bonds

•

environmental policy

•

environmental studies

•

financial management

•

flood insurance

•

flood studies

•

insurance

•

markets

•

NFIP

•

Friday January 01, 2016

Flood Mitigation Mistakes in Tucson

•

disaster management

•

environmental policy

•

environmental science

•

environmental studies

•

flood studies

•

insurance

•

NFIP

•

risk management

•

2015

Tuesday December 29, 2015

Review on Government-Run Disaster Risk Pools

•

disaster management

•

disaster risk

•

environmental policy

•

environmental studies

•

flood studies

•

natural disasters

•

NFIP

•

risk management

•

Thursday December 10, 2015

Don't Cancel Flood Insurance due to Mitigation

•

environmental policy

•

environmental studies

•

flood insurance

•

flood mitigation

•

flood studies

•

NFIP

•

Thursday November 19, 2015

Whistling tunes we hide in the dunes by the seaside

•

beach replenishment

•

environmental justice

•

environmental policy

•

environmental studies

•

flood mitigation

•

NFIP

•

Tuesday November 10, 2015

Social Benefits of Voluntary Buyouts Following Flooding

•

environmental policy

•

environmental studies

•

flood mitigation

•

NFIP

•

risk management

•

Saturday September 26, 2015

Flooding Risk and Environmental Justice

•

environmental justice

•

environmental policy

•

environmental studies

•

flood studies

•

NFIP

•

social justice

•

Wednesday July 01, 2015

Valacer's Article on the NFIP

•

environmental policy

•

environmental studies

•

flood studies

•

NFIP

•

recent research

•

Friday June 05, 2015

Wealthier Communities Pay Less for Flood Insurance

•

CRS

•

environmental policy

•

environmental studies

•

FEMA

•

flood insurance

•

flood studies

•

NFIP

•

Tuesday June 02, 2015

Reforming the NFIP

•

disaster management

•

economics

•

environmental policy

•

environmental studies

•

flood insurance

•

flood studies

•

NFIP

•

Wednesday March 04, 2015

An Individual Mandate for Flood Insurance

•

behavioral economics

•

economics

•

environmental policy

•

environmental studies

•

flood insurance

•

flood studies

•

NFIP

•

public affairs

•

public policy

•

2014

Saturday November 15, 2014

Flood Insurance Pricing

•

behavioral economics

•

environmental policy

•

environmental studies

•

flood insurance

•

flood studies

•

NFIP

•

pricing

•

Friday October 31, 2014

The NFIP and Florida

•

climate change

•

environmental policy

•

environmental studies

•

flood studies

•

Florida

•

insurance

•

NFIP

•

Monday June 16, 2014

Introducing Flood Studies

•

environmental policy

•

environmental science

•

environmental studies

•

flood insurance

•

flood studies

•

NFIP

•

research

•

Monday March 31, 2014

Slides for my Dissertation Defense

•

dissertation

•

environmental policy

•

environmental studies

•

flood insurance

•

NFIP

•

UMBC

•

2013

Friday February 22, 2013

Slides from SBCA

•

conferences

•

dissertation

•

environmental policy

•

environmental studies

•

flood insurance

•

NFIP

•

Tuesday January 01, 2013

Presenting "Estimating the Net Social Benefits of the NFIP" at the Benefit-Cost Society Conference in Februrary

•

benefit-cost analysis

•

environmental policy

•

environmental studies

•

flood insurance

•

flood mitigation

•

flood studies

•

NFIP

•

research

•

UMBC

•

2012

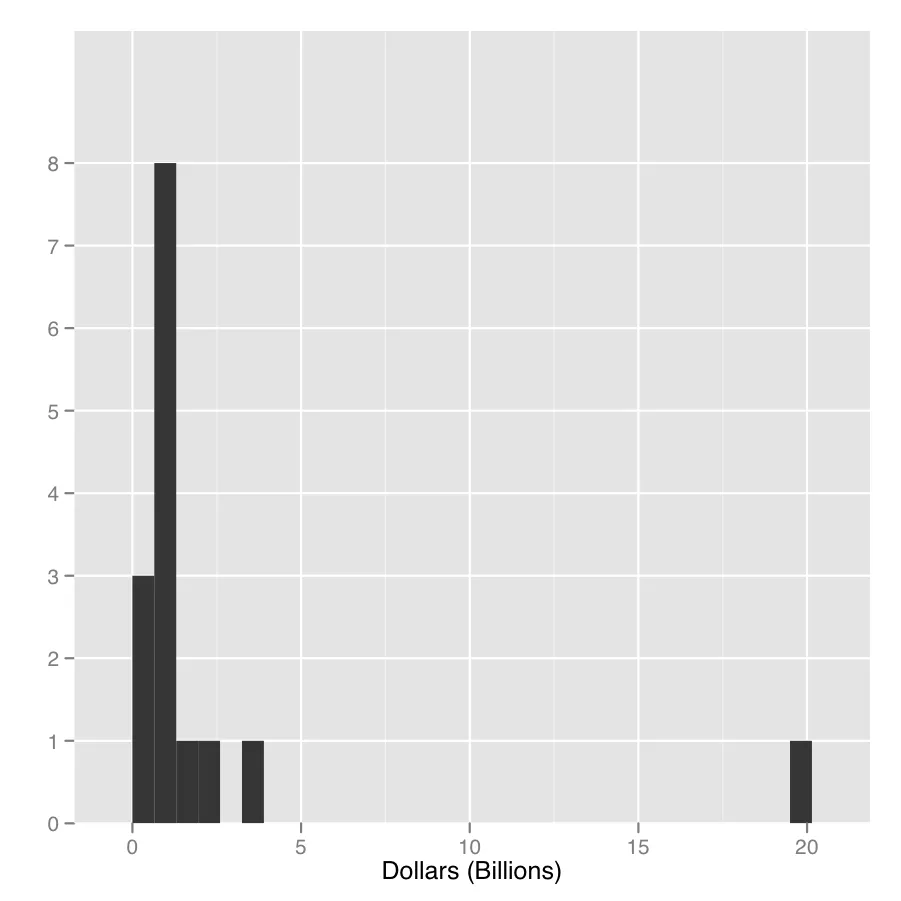

Wednesday September 19, 2012

Flood Insurance Claims

•

disaster management

•

environmental policy

•

environmental studies

•

FEMA

•

flood studies

•

NFIP

•

Saturday March 24, 2012

Measuring the Impacts of the National Flood Insurance Program

•

benefit-cost analysis

•

environmental policy

•

environmental studies

•

flood insurance

•

flood mitigation

•

flood studies

•

NFIP

•

UMBC

•

wmgrs

•

Sunday January 22, 2012

Dissertation Proposal Defended

•

benefit-cost analysis

•

dissertation

•

environmental policy

•

environmental studies

•

flood insurance

•

flood mitigation

•

flood studies

•

NFIP

•

UMBC

•

Saturday January 21, 2012

Dissertation Proposal Defense Slides

•

dissertation

•

environmental policy

•

environmental studies

•

flood insurance

•

NFIP

•

UMBC

•

Tuesday January 10, 2012

Talk on the NFIP at the Graduate Research Symposium

•

environmental policy

•

environmental studies

•

FEMA

•

flood insurance

•

flood mitigation

•

flood studies

•

NFIP

•

UMBC

•

wmgrs

•